These texts present a more in-depth reasoning about, and a complement to, selected parts of NRIA Flyg 2024.

Supplement A: Propulsion alternatives for fossil-free aviation

Sustainable hydrocarbon fuels (SAF) – general

+ Drop-in.

+ Already certified for up to 50%, in some cases up to 100%. No major modifications of aircraft or engines are needed, which in itself saves significant global resources.

+ Can be customised for lower particle emissions by reducing the content of long or aromatic hydrocarbons.

– Produces NOx emissions (nitrogen oxides) and contrails during high-altitude flights. However, research shows that there are fewer soot particles and thus fewer contrails with SAF compared to fossil fuels, especially if tailored to shorter, non-aromatic hydrocarbons.

Large quantities of SAF will be needed, and it is therefore essential for many countries to contribute to their own SAF production – including Sweden. The competition for fuel will be significant, especially from the road-vehicle sector. However, for road vehicles, battery operation represents a solution to a much greater extent than in aviation, meaning that aviation could be given higher priority than road traffic as a SAF market.

ICCAIA, which is a global association of various aviation-industry lobby groups, published a commitment proposal in September 2023 stating that all civil aircraft in production should be able to operate on 100% SAF by 2030. Currently, a maximum of 50% SAF is certified and allowed. This is a positive signal indicating that the aviation industry is prepared and proactive.

SAF-bio (biofuel)

Refers to synthetic liquid hydrocarbons made from biomass and, in some cases, also hydrogen.

+ Several have already been certified.

– More expensive than fossil fuels. Fuels based on various bio-oils (tall oil, palm oil, rapeseed oil and similar) have limited raw-material availability. Fuels produced from gasified biomass (primarily from logging residues, known as “grot” – branches and tops) using Fisher-Tropsch/GTL (gas-to-liquid) are even more expensive than bio-oil-based fuels, but there is an abundance of raw material available. New liquid-based processes from grot to oil are also being developed.

SAF-PTL (Power-to-liquid)

Refers to liquid hydrocarbon fuel synthesised from carbon dioxide and hydrogen (using electricity).

+ Can use captured carbon dioxide as a raw material.

– Underdeveloped manufacturing process.

– Likely consumes a very high amount of electricity during fuel production (much higher than the electricity consumption for the electrolysis of hydrogen).

Hydrogen

Hydrogen is an attractive fossil-free fuel that can be produced through the electrolysis of water. Hydrogen has a high energy density concerning mass (Wh/kg) but low density in terms of volume (Wh/m3). Pressurised tanks are limited to very small aircraft, as they become too heavy when scaled up. For larger aircraft, cryogenic hydrogen is required, which means cooling the hydrogen to –253°C to turn it into liquid and storing it in tanks similar to large thermoses. It is likely that it will be practical to produce hydrogen near airports, which could lead to airports becoming hubs for refuelling hydrogen-powered ground vehicles as well.

Hydrogen – combustion in gas turbine engines

+ Cheaper than electro-fuels.

+ Well-established production through the electrolysis of water.

+ Produces zero carbon-dioxide emissions when used.

+ More energy-dense than hydrocarbon fuels in terms of weight.

+ Easy to combust in a gas-turbine engine.

– Not a drop-in fuel.

– Approximately four times lower energy density in terms of volume (Wh/m3) than hydrocarbon fuel.

– Requires cryogenic tanks and a new fuel system, which is a technical challenge.

– Produces nitrogen oxide emissions and water vapor but no particles. Research is needed to assess high-altitude effects, but it is likely better than hydrocarbon fuels since the latter generate particles required for the formation of contrails. Furthermore, the water vapor from contrails has a much shorter “lifetime” in the atmosphere, which allows the high-altitude effect to dissipate faster.

Hydrogen – fuel cells

+ No carbon dioxide, only water vapor as emissions.

+ No nitrogen-oxide emissions.

+ Higher energy density in terms of mass (Wh/kg) than batteries.

– It is a technical challenge to scale up to high outputs and large aircraft. Development is needed to achieve higher power density concerning mass (W/kg). It is challenging to attain sufficient acceleration and maintain a high flight speed. It may work for smaller planes on regional routes, but the low flight speed likely limits interest in flying fuel-cell aircraft over longer distances.

– Auxiliary systems are needed to cool the fuel cells (which get very hot). These tend to be heavy and complicated (compared to a jet engine that “cools itself” through the incoming air).

Batteries – electric aviation

+ Established technology for road vehicles.

+ High efficiency.

+ Simple and robust system.

– Primarily low energy density concerning mass (Wh/kg) in today’s batteries, resulting in heavy aircraft and short range. There is also some uncertainty regarding battery lifespan.

Electric hybrid

In this area, several different solutions with varying degrees of hybridisation are being studied. Common to all is that they require SAF or hydrogen to be fossil-free.

-

- More electric/micro-hybridisation: More electricity is generated for various onboard systems or to optimise the jet engine (redistributing work between modules).

- Series hybrid: Gas turbine – electric generator (possibly battery) – several electric motor-driven fans/propellers, providing a higher propulsion efficiency as the gas turbine drives more than one fan (to levels exceeding the highest possible bypass ratios for a directly driven fan/propeller).

Different architectures with various-sized batteries. - Parallel hybrid: Several potential solutions where a gas turbine or turboprop engine is arranged in parallel with an electric drivetrain. The Swedish company Heart Aerospace is studying such a concept.

- • Hybrid solutions including hydrogen fuel cells.

Lower energy consumption

Note that technologies for lower energy consumption, such as more efficient engines, lighter structures, or new aircraft configurations, represent the largest measured contribution to date in reducing aviation’s climate impact. This technological pathway is expected to remain important for a long time and will become even more crucial with the high cost of SAF or hydrogen. Read more about this in NRIA Flyg 2020.

Supplement B: Future fuels for aviation within and from the EU

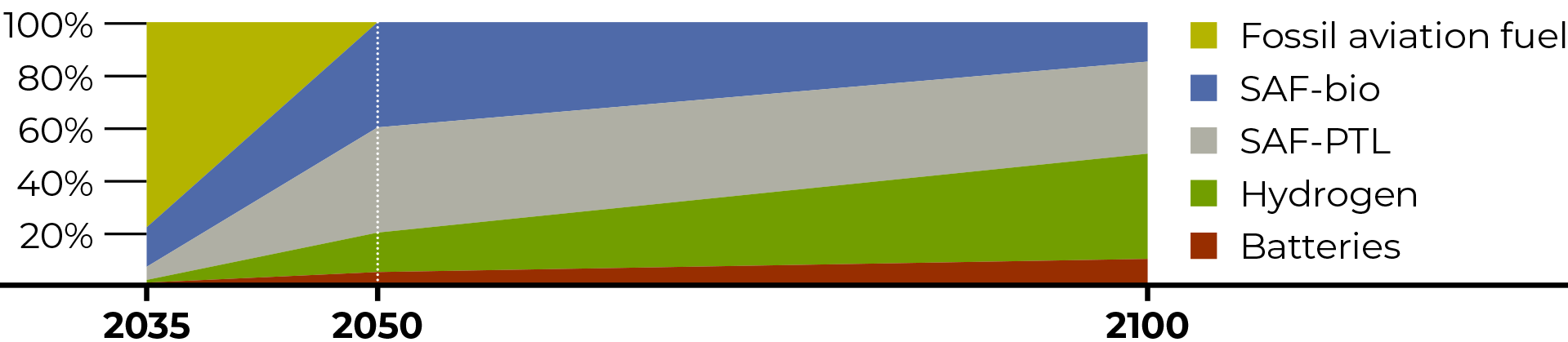

How quickly can we expect global aviation to transition to fossil-free propulsion? And what type of energy carrier will emerge first? Here, Innovair presents a projected distribution among the various types of energy carriers for the years 2035, 2050 and 2100.

Figure: Innovair’s forecast for future fuels for aviation within and from the EU. (EU goals: 2030: 6% SAF; 2050: 70% SAF.)

The use of biofuel blends (SAF-bio) is already increasing. This fuel is expected to be initially important and become the largest fossil-free fuel by 2035, after which SAF-PTL is anticipated to gradually take over up to 2050. Hydrogen is likely to be introduced first in regional aviation, with plans to expand into the medium-haul segment by 2050 and become the dominant aviation fuel by 2100, alongside SAF-PTL, which will likely still be needed for long-haul flights.

As we showed in NRIA Flyg 2020, it is not only disruptive technological shifts that will move the world toward the climate goals. The continuous development of more efficient and lighter aircraft and engines that leads to reduced fuel consumption, along with the ongoing replacement of old aircraft with new ones, provides a significantly measurable contribution, resulting in decreased emissions of up to 1.5% per passenger kilometre annually. Accumulated, this leads to a substantial reduction in total emissions from aviation.

Supplement C: Fuel production

Civil aviation, the Armed Forces and the overall Swedish defence (Totalförsvaret) will be highly dependent on liquid fuels for a long time. The challenge lies in implementing a transition to fossil-free fuels while ensuring national fuel supply. According to industry actors, production itself is a limited problem; the bottleneck is financing the development of large-scale production facilities. Commercial actors find it difficult to assume the financial risk, and where funding is available, necessary government guarantees for future utilization of the produced fuels are lacking.

An additional sustainability parameter is the transportation of the large quantities of aviation fuel needed at our airports. In this context, it becomes relevant to discuss the role of airports in the logistics system for aviation fuel. Where should production facilities be located, and how should storage solutions be planned?

Internationally, there is investment in fossil-free aviation fuel, both biofuels and electrofuels. The fact that the industry successfully certified a blend of up to 50% biofuels in existing technology as early as 2009[1] indicates significant foresight on the issue. Today, there are seven certified pathways for the production of biofuels. The blending requirements are gradually increasing. However, there are significant uncertainties in the cost estimates for producing fossil-free alternatives, particularly in terms of electricity prices and raw material availability.

Fossil-free aviation fuels will, for a long time, be benchmarked against the price development of regular crude oil. All of this is part of the equation that airlines must consider when purchasing aviation fuel. Airlines currently operate with (very) narrow margins in their businesses. The speed of civilian sector transition will largely depend on international regulations and incentive structures.

Technically, the requirements for the next generation of civil and military propulsion systems need to accommodate a development where a broader spectrum of fuels can be used while maintaining flight safety and performance.

There are many directives that govern the climate-related transition of aviation, and within Sweden, all relevant actors must collaborate to meet them. We see this agenda as a means to describe the challenges, and we provide certain recommendations. The responsibility for adhering to the directives and achieving the goals then lies with actors in the public sector, industry and academia.

The challenges are common to all associated nations, and we see that active participation in joint programmes is a primary course of action. To gain access to this work, we need to maintain the national investments in collaboration and competence building that have been manifested over the years through NFFP and Innovair.

At the Swedish level, research is being conducted to find the most optimal conditions for Swedish SAF production concerning carbon sources, fuel composition and combustion properties. The research is led by the Competence Centre in Sustainable Turbine fuels for Aviation and Power (CESTAP), a newly established centre that includes academic and industrial partners promoting the production and use of sustainable fuels for stationary gas turbines and jet engines. Academic and institute partners include Lund University, Luleå University and RISE (Research Institutes of Sweden). CESTAP is funded by the Swedish Energy Agency, with contributions from around 25 industry partners and academic institutions. Another Swedish initiative is TechForH2, a competence centre for multidisciplinary hydrogen research at Chalmers. Both these initiatives contribute to competence development of great significance for Sweden’s competitiveness in international efforts focused on sustainable aviation.

[1] IATA Fact Sheet 2 – Sustainable Aviation Fuel: Technical Certification.

Supplement D: Circularity

The aviation industry has a long tradition of dismantling decommissioned aircraft and reusing various parts. However, the increased use of carbon-fibre composites in aircraft presents certain challenges compared to aluminium, which is currently reused to a high degree. Within the EU programmes Clean Sky 1 and 2, some of the subprogrammes have focused specifically on sustainability, resource-efficient design and manufacturing methodologies. Eco-fibres, environmentally friendly matrix materials and the reuse of carbon-fibre composites have been studied. The entire lifecycle from design to recycling/reuse has been analysed, to enable the right measures to be taken in the design process.

New manufacturing processes such as 3D printing reduce material consumption, and less material needs to be recycled as these methods entail nearly no post-processing. This can be compared with traditional machining, which today results in up to 90% material removal, but where all removed material is handled and returned to the smelters.

Today, the industry is more aware, and the major OEMs have high ambitions for the next generation of aircraft, which should be much more easily dismantled to allow the largest possible amount of material to be recovered and reused.

Within the industry, there is an increasing focus on life cycle assessment (LCA). The focus is not only on circularity but also on the entire chain, from the origin of the raw materials (ensuring that the raw materials are not conflict minerals) to end-of-life disposal.

Supplement E: Airspace

In the main document NRIA Flyg 2024, several factors that are central to the aeronautics industry’s focused efforts to achieve climate and environmental goals by 2035 and 2050 are described. Some of these are directly linked to how we utilise airspace and to the regulations and ordinances necessary for safe aviation. At the same time, the requirements for airspace management are changing, partly due to new categories of aircraft and the influence of society’s rapid digitalisation.

The development needs within Swedish airspace and its infrastructure have thus increased. We already have a large number of actors utilising the airspace, and we see that the number of new actors is increasing rapidly. Examples include drones, manned and unmanned vehicles for electrical vertical take-off and landing (eVTOL) and electric aviation. The development regarding both electric aircraft (battery, hydrogen, hybrid) and autonomous vehicles is progressing quickly, and with technological advancements, the number of applications and airspace users for these will also increase. We can most likely expect to see new patterns of movement and traffic flows in the air, given that these new vehicles have different performance characteristics and ranges compared to today’s conventional aircraft. New flight paths and several short stops may lead to increased traffic and passenger volumes at smaller regional airports. For a deeper analysis of these conditions, refer to the chapter ” Aviation’s Environmental and Climate Impact ” in NRIA Flyg 2020.

The international security situation imposes further requirements for robust services and systems for air-traffic control and infrastructure. It also leads to increased presence with exercises in the airspace for both the Armed Forces and emergency-service-related actors. Sweden’s entry into NATO further enhances defence-related exercise activities in Swedish airspace.

Supplement F: European collaboration related to the defence sector

EU Capability Development Priorities

Since 2008, the EDA has regularly updated a Capability Development Plan (CDP). Given the heightened global security situation, it has increased in significance and has served since the end of the 2010s as a foundation for defence-related EU instruments such as EDF, PESCO and CARD. The intent is that, together with the strategic compass, NATO’s regional planning, and more, it will serve as a primary reference for coordinating the national capability development of member states.

For the air domain, the 2023 edition focuses on:

-

- Air-combat capability including upgrades of existing platforms, next-generation combat aircraft (manned and unmanned), development and integration of armed UAVs, and next-generation airborne precision weapons.

- Airborne C4ISTAR[2] capability including both manned and unmanned flight systems.

- Integrated Air and Missile Defence (IAMD[3]) including both existing and newly developed air-defence systems, including systems for countering drones and hypersonic missiles.

- Aerial transport systems including unmanned tactical transport, next-generation helicopters, systems for air refuelling, and the next generation of manned aircraft for tactical and strategic transport.

EDF with PESCO and CARD

Within the EU, there is a rapid increase in ambition, which is manifested, among other things, in the European Defence Fund (EDF). With a budget of €7.9 billion for the period 2021–2027, the fund aims to strengthen and consolidate the European defence industry to reduce dependence on non-European resources and to secure the military capability growth needed within the EU.

Linked to the CDP (see above) is the EDA instrument Coordinated Annual Review on Defence (CARD), which aims to propose and guide collaboration within PESCO, EDA, EDF, or bilaterally, based on gap analyses and the plans of member states. Another instrument is the Permanent Structured Cooperation (PESCO), aimed at identifying and harmonising common capability needs and establishing multinational collaborative projects.

The EDF presents a significant opportunity for Sweden to enhance the national innovation system related to defence and dual-use-related technology development. Sweden has already achieved notable success in influencing program orientation toward areas relevant to Swedish interests and in securing EU funds for Swedish defence industry and research actors. However, there is still development potential in this area, where a more structured approach could increase Sweden’s ability to influence the programme’s long-term direction and initiate collaboration to support Swedish capability development and agility in swiftly evaluating and leveraging initiatives from other member states.

The EDF also has industrial policy goals aimed at strengthening European defence industry from a socio-economic perspective. The connection between military utility, high-tech industry with potential spin-offs into other sectors, and economic growth is evident and has further potential to be exploited.

This does not only present opportunities, as the EDF aims to eventually develop military materiel (equipment and supplies). Materiel development within the EDF occurs through a series of projects with gradually increasing TRL and thus requires increased funding from participating countries. This also includes commitments from participating countries to purchase the developed material. In the long term, this could mean that Swedish companies are excluded from part of the market if they are not involved in these development projects. Experience shows that it is difficult to enter subsequent projects if a company has not been involved from the start.

EDF calls for proposals are issued annually in the first quarter, with deadlines for project proposals in the late autumn. Allocation decisions are made during the spring of the following year.

“Input” to the EDF

Sweden’s ambitions in the EDF include influencing the direction of the fund to align with development areas that match both Swedish capability needs and the strengths and focus areas of Swedish industry.

Since EDF is based on international cooperation, Sweden must coordinate internally to ensure participation in areas where we can contribute effectively. There is a need to influence both overall program direction and specific calls for proposals, as well as to synchronize national project proposals – all to ensure Swedish presence in development.

Typical areas that Sweden wants to see more of, and obtain contracts in, include:

-

-

- Collaborative systems;

- Capability to detect/identify threats and targets and create information superiority;

- Survivability;

- Command, control and communication;

- Autonomy;

- Weapon effects and protection;

- Propulsion;

- Advanced materials;

- Electricity generation;

- “Distributed” Global Eye;

- “Automated” preparation of aircraft (in a distributed system);

- Software updates for relatively static hardware.

-

EDA

The European Defence Agency (EDA) is an intergovernmental authority in Europe aimed at promoting cooperation and initiating new efforts to improve Europe’s defence capacity. EDA provides a legal framework for contracting industries on behalf of member states and coordinates follow-up activities. EDA also has the ability, within its operational budget, to commission studies and organise workshops, often leading to new projects or topics that can be announced as EDF calls.

In addition to its previously described roles in CDP, CARD and PESCO, EDA is responsible for the Overarching Strategic Research Agenda (OSRA), which is based on underlying strategic research agendas developed by the EDA’s Capability Technology Groups (CapTech groups) consisting of experts from agencies, industry, SMEs and academia. There is a dedicated CapTech for aerial systems, but several other CapTechs indirectly relate to the aeronautics sector. These strategic research agendas are expected to have a significant impact on the content of work programmes and long-term plans within the EDF. Therefore, active and broad Swedish engagement in EDA’s CapTech groups is crucial.

NATO

Sweden’s membership in the NATO defence alliance will impose new requirements on the development of Swedish defence capabilities, not least within the aviation domain. Currently, these requirements are only outlined in an interim version[4] and are subject to analysis and interpretation. They are part of the conditions for the previously mentioned operational concepts developed within the Swedish Armed Forces. Upcoming defence decisions will include specific changes and re-planning prompted by NATO membership.

The altered demands on Swedish air power capacity create new challenges concerning aeronautics technology development. We are transitioning from having a national air force tailored primarily for defensive air defence to becoming a component of an alliance with common deterrence as a strategy. The potential area of operations will suddenly become significantly larger, and the tasks will expand to include contributing to a credible offensive capability in areas adjacent to other NATO countries.

NATO’s strategy to address increased threats in the world is manifested, among other things, in the development of the previously mentioned Integrated Air and Missile Defence (IAMD). Sweden’s anticipated role in this is to serve as a crucial piece of the puzzle. New operational concepts for IAMD are under development, where full interoperability – operationally and technically – with NATO’s air-combat forces and missile defence is a fundamental prerequisite.

Within the alliance, there are several planning processes[5] in which Sweden will participate. The results of these processes will influence and guide the future direction of Swedish defence development.

Parallel to EDF, NATO’s Defence Innovation Accelerator for the North Atlantic (DIANA), aims primarily to foster cooperation with and support the best and most innovative technology companies and researchers within the alliance, in order to leverage their – possibly originally civilian – innovations for defence purposes. DIANA is complemented by the NATO Innovation Fund (NIF), which is a multinational venture-capital fund for start-ups and scale-ups developing technologies in defence and security. The Swedish government intends to invest just over 400 million SEK in this fund.

Within NATO, there is also the Science and Technology Organization (STO), with participation from member states and partner countries. STO is divided into six Technical Panels, each focused on activities relevant to the participating parties. In addition to the six panels, there is a special group dedicated to modelling and simulation. Sweden, as a highly valued partner country, has participated for many years, with representatives from several of our defence agencies and the defence industry.

With Sweden’s NATO membership, increased Swedish participation in these programmes offers significant potential to strengthen our defence and innovation capabilities.

Other international collaboration

Sweden has, related to NRIA and also directly linked to Innovair’s internationalisation efforts, active project collaboration with Brazil, the United Kingdom (UK) and Germany. Since 2015, the most extensive collaboration has been with Brazil, where several projects – many funded through NFFP – have been conducted under an umbrella referred to as the Air Domain Study. This collaboration also includes a comprehensive program of guest professors, post-docs, PhD candidates and other mobility activities, where the Swedish Armed Forces Research Centre (SARC) has played an important role.

The collaborations with Brazil, the UK and Germany target both sustainable aviation and societal security, involving components related to testing accelerated technological development. Bilateral projects in the aeronautics sector also exist between FMV/FM and, for example, USA, and these have been ongoing for many years.

Given the current security policy environment, there is an increased need to think critically and apply a holistic perspective when engaging in foreign collaborations that may have military applications.

[2] C4ISTAR: Command, Control, Communications, Computers, Intelligence, Surveillance, Targeting Acquisition and Reconnaissance).

[3] IAMD: Integrated Air and Missile Defence.

[4] ICD (Interim Capability Targets 2022) will transition to CT25 following NATO entry and as a result of the NDPP’s planning cycle.

[5] Nato Defence Planning Process (NDPP).